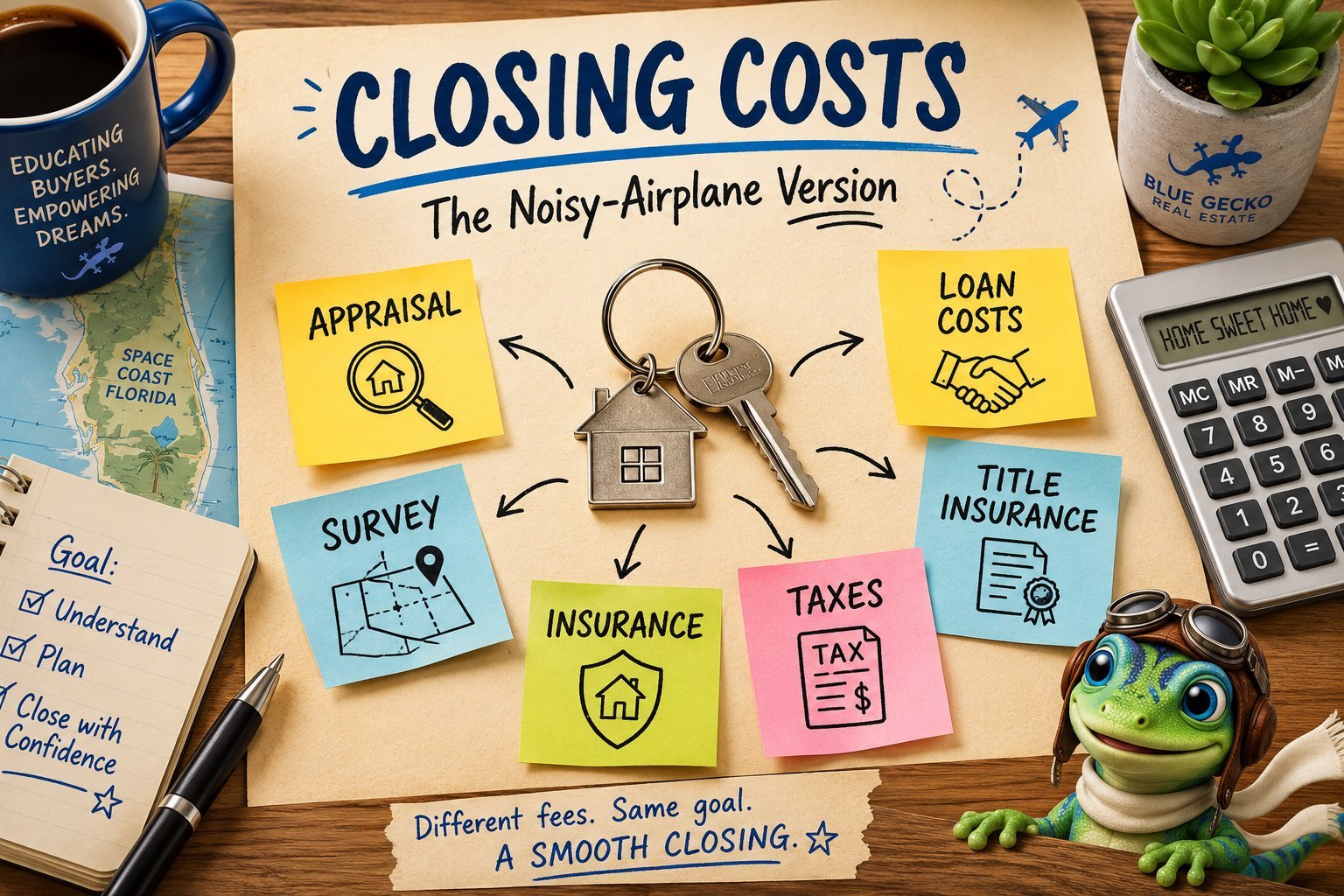

Closing Costs: The Noisy-Airplane Version

Closing costs are the collection of fees and expenses required to complete a home purchase. They typically include lender fees, appraisals, title work, insurance, taxes, and government recording fees.

If that sounds a little overwhelming, don’t worry.

Closing costs are one of those things every homebuyer hears about, but nobody really explains until you’re halfway through the mortgage process and staring at a stack of paperwork.

For this article, we’re going to keep things simple. Think of this as the version you could explain to the person sitting next to you on a noisy overnight flight while the engines are roaring and neither of you got enough sleep.

We’re going to stay at the 30,000-foot level and focus on what these costs are and why they exist.

Closing Costs at a Glance

Most financed home purchases include some combination of:

- Loan Costs

- Appraisal Fee

- Title Insurance

- Survey

- Recording Fees

- Homeowners Insurance

- Property Taxes

- Escrow Account Funding

- HOA or Condo Fees

Now let’s talk about what those actually mean.

Loan Costs

Imagine walking into a bank and asking to borrow $400,000.

The bank doesn’t just smile and hand over a check. A whole team of people starts researching both you and the property. They check your credit, verify your income, review your paperwork, make sure the seller actually owns the home, and look for any legal issues that could create problems later.

All of that work takes time and expertise. Some of the fees you’ll see at closing are simply the cost of the people and companies doing the research necessary to get everyone comfortable saying, “Yep, let’s do this.”

Appraisal Fee

Let’s say you want to buy a collectible for $10,000.

Before loaning you the money, the bank would probably want someone to confirm that the collectible is actually worth $10,000. Homes work the same way.

An appraiser compares the property to recent sales and market data to determine its value. The bank wants to make sure the house is worth what you’re paying before they lend against it.

Title Insurance

Even after all the research is done, weird things can happen.

Missing paperwork. Old recording mistakes. Long-lost heirs. Forgotten easements. Possibly an ancient burial ground that somehow never made it into the county records.

Human beings have been making filing errors for a very long time.

Title insurance protects you and the lender if one of those old ownership issues unexpectedly surfaces after you buy the home.

Survey

A survey answers a pretty simple question:

“Exactly what am I buying?”

It confirms property boundaries and can identify things like fences, easements, or structures that cross property lines. Here on Florida’s Space Coast, surveys are also commonly used to help verify flood zone information, which can affect both insurance requirements and future building plans.

Think of it as a map that helps everyone understand exactly what is being transferred before ownership changes hands.

Recording Fees

Once the sale is complete, somebody has to make it official.

Recording fees are paid to the county so the deed and mortgage can be entered into the public record. In simple terms, it’s the government’s fee for updating the paperwork to show you’re the new owner.

Homeowners Insurance

The day you become a homeowner is also the day you become responsible for everything that happens to the home.

Because of that, lenders require insurance coverage to be in place before closing. In many cases, the first year’s premium is collected upfront so you’re protected from day one.

Property Taxes

Property taxes don’t stop just because ownership changes.

Depending on when you buy, you may need to pay a portion of upcoming property taxes at closing. This isn’t an extra charge as much as it is making sure everyone pays their fair share of the tax bill for the time they owned the property.

Escrow Account Funding

This is the one that causes a lot of confusion.

Many lenders collect a few months of future taxes and insurance payments upfront and place that money into an escrow account. Later, when those bills come due, the lender pays them from that account on your behalf.

Think of it like setting money aside for future expenses before they arrive.

HOA and Condo Fees

If you’re buying in an HOA or condo community, there may be application fees, transfer fees, capital contribution fees, or prepaid dues collected at closing.

Every community has its own rules and fee structure, so this is one area where costs can vary quite a bit from one property to another.

Frequently Asked Questions

What are closing costs?

Closing costs are the fees and expenses associated with purchasing a home beyond the purchase price itself. They often include lender fees, appraisals, title work, insurance, taxes, and government recording fees.

Are closing costs the same as a down payment?

No. Your down payment goes toward the purchase of the home. Closing costs are separate expenses required to complete the transaction.

Who pays closing costs in Florida?

Both buyers and sellers typically have closing costs, although the exact costs paid by each party can vary based on the contract and local customs.

Can closing costs be negotiated?

Sometimes. Sellers may agree to contribute toward a buyer’s closing costs as part of the purchase agreement.

Do cash buyers pay closing costs?

Usually yes, although cash buyers often avoid many of the lender-related fees discussed in this article.

Lucky’s Take

Most closing costs exist because somebody is checking, verifying, insuring, recording, or protecting something.

The names may change. The paperwork may get thicker. But at the end of the day, closing costs are simply the collection of expenses that help make sure everyone gets what they think they’re getting.

And if somebody starts explaining closing costs using twenty-seven mortgage acronyms in a row, feel free to stop them and ask for the noisy-airplane version instead.

About the Author